With the release of X_STUDY® 7.8.0, users of our charting application can now apply a technical indicator (or study) to the value of another technical indicator. Although this feature can be used in many ways, two primary ways are to help measure market conditions and increase or improve trading signals. I’ll show a few simple examples of this feature, which we call study on study.

Measuring Market Conditions

A classic study on study is to place a moving average on the volume indicator. Averaging the last few volume bars helps to gauge what kind of tempo the market is experiencing relative to the past. In addition, volume levels are compared to averages, especially at highs and lows.

|

| Figure 1: One-minute September E-mini S&P 500 chart |

Figure 1 above shows a chart with a red moving average placed on the volume indicator. Notice I also added a second study on study with an orange max indicator applied to volume. This max study simply finds the maximum value over the user-defined look-back period. Both the simple moving average and the maximum indicators are looking back 20 bars.

Continue Reading →

Tags: Charting

As I mentioned in my last blog, X_STUDY® charts offer more than traditional bar data. Along with the open, high, low, close and volume for each bar, we have a list of volume at each traded price. This list is commonly referred to as Volume at Price, or VAP, and can be visually displayed on an X_STUDY chart. The VAP data is then used to calculate many key technical price levels like Volume Weighted Average Price (VWAP), Volume Point of Control (POC) , Value Area High (VAH) and Value Area Low (VAL).

VAP

Let’s look at VAP before we explain these important daily price levels. VAP is generally plotted on a chart to view which price levels have attracted high-volume trading and which price levels have relatively low volumes. These high- and low-volume areas often form bell-shaped curves turned on their side, and are commonly referred to as volume profiles.

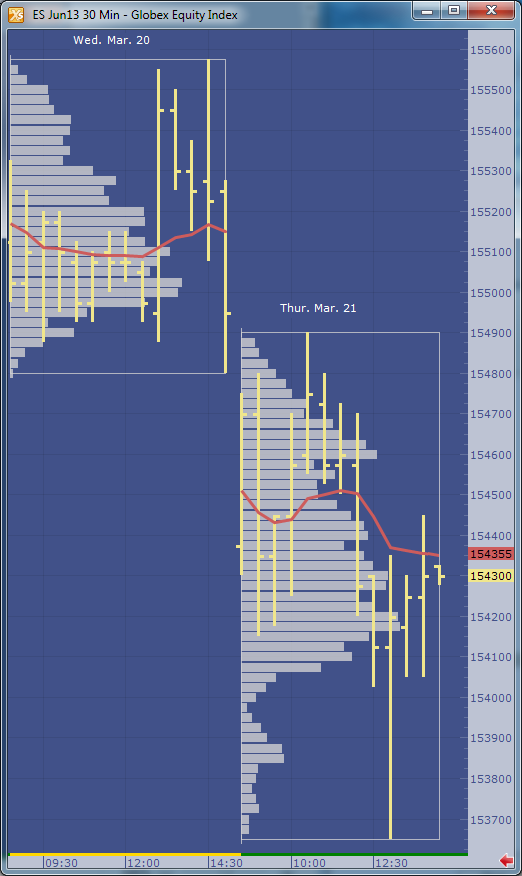

Figure 1 shows an example of the profile made on a 30-minute bar chart with the VAP indicator configured to group each daily session. I am using X_STUDY 7.8, which we just released. This version has the ability to display the volume labels at each price, as in Figure 1 below.

|

| Figure 1: June 2013 S&P E-mini contract with daily VAP groups. |

In evaluating volume profiles, one can apply principles similar to

Market Profile® theory. VAP can show additional details not found in profile analysis, too. Look at Figure 1 on March 21. There was a single 30-minute bar forming the day’s low. Notice the heavy volume at 1538.50 and 1538.75 compared to the other price levels during this 30-minute period. This is something you could not see with a standard chart or a Market Profile chart.

VAP Calculations

Now on to the calculations that are derived from VAP. One of the most highly used calculations from VAP data is the Volume Weighted Average Price, or VWAP. This calculation sums the results of the volume at each price multiplied by the price, then divides the sum by the total volume over the interval. You can see the formula here.

In Figure 2 below, we add the VWAP to the chart. This red line shows how the VWAP developed through the day. You will often find high-volume trading and good support and resistance at these levels since this value is used as a benchmark at many large trading institutions.

|

| Figure 2: Daily VWAP added to the chart. |

Figure 3 adds the maximum VAP, or Volume Point Of Control (POC), to the chart. This is simply the price that has the highest volume value for the defined group. Notice I called this Volume POC. If you are familiar with Market Profile charts, you know they too have a POC based on Time Price Opportunity (TPO) count. I’ll save these charts for a later blog.

|

| Figure 3: Maximum VAP, or Volume POC, highlighted in yellow. |

The next calculation is going to be a little harder for me to explain without this blog becoming too lengthy, but I’ll give it a try. Value area, or volume value area since these calculations are going to be done on the VAP dataset, is an algorithm that calculates 70 percent of the volume. I rounded up to 70 percent from the original standard deviation worth of volume, which was 68 percent.

The algorithm starts by finding the volume POC, then adds two volume price levels above or two volume price levels below the POC to the value area. We add the group with the largest volume. For example, if the two price levels above the POC add up to 10,000 volume and the two price levels below add up to 9,500 volume, then we add the top two price levels to the value area. The 9,500 will then be compared to the sum of the next two VAP values above the 10,000 group. Again, the larger of the two amounts is added to the value area. The algorithm continues adding volume groups until reaching 70 percent of the volume.

|

| Figure 4: The value area is highlighted in green. |

In X_STUDY, the VAP indicator is highly customizable. For example, if you want to highlight only 50 percent of the volume for the value area calculation, you can simply change it in the VAP indicator properties. If you want to change the grouping for the VAP, you can do that too.

See Figure 5 for a fast-action volume profile chart. This is a two-minute bar chart with VAP group size of 15. We are now grouping or displaying the volume profiles for each 30-minute bar. The chart also displays the daily VWAP and TT CVD® indicators.

|

| Figure 5: A faster VAP indicator setup. |

X_STUDY® 7.8.0 Release

This concludes X_STUDY’s extended set of market data points; but wait, there’s more! With the new release of X_STUDY 7.8 on May 8, we have exposed the above additional calculations for each bar to be used by all of the technical indicators.

That’s right, each bar now has a VWAP, maximum VAP, value area high and low along with the open, high, low and close. This revolutionizes all of X_STUDY’s technical indicators. We haven’t changed the formulas for the existing indicators. We are simply exposing these new bar data points, which are a little more intelligent.

For example, a simple moving average is generally calculated on each bar’s closing price. Now X_STUDY users can choose to use the maximum VAP instead of the close for the bar. How about a 50-day VWAP moving average instead of a 50-day closing price average?

How about using the stochastics indicator and defining the high as the value area high, the low as the value area low, and the close as the maximum VAP of the bar? This turns the stochastic indicator into a stochastic indicator based on each bar’s value area instead of the bar’s high and low.

I could go on and on here, but I will stop now. I’ll be showing more features of X_STUDY 7.8 in my next blog. Until then, I hope the above feature sounds interesting and leads you to try our latest release of X_STUDY.

Tags: Charting

X_STUDY charts offer more than traditional bar data. Along with the open, high, low, close and volume for each bar, X_STUDY provides additional data points, like the total number of market sellers hitting the bid, or bid volume, and the total number of market buyers lifting the offer, or ask volume. As explained in my last blog, these bars can be time-based or volume-based.

Today I’d like to talk about TT CVD, a true leading technical indicator that works off these powerful market data points.

You might be thinking: “All technical indicators are lagging indicators.” But after you see how TT CVD is calculated, you will probably agree that this is a leading indicator. It can complement just about any trading strategy, too.

TT CVD Overview

TT CVD uses the bid and ask volume data to display the running difference of the ask volume (the market buying pressure) minus the bid volume (the market selling pressure)—or, in short, the cumulative volume delta (CVD). Let’s walk through a real-world example to illustrate how TT CVD is calculated.

Figure 1 below shows a chart of the December E-mini S&P 500 contract with three studies. The first, Volume Delta—Histogram, displays the total bid and ask volumes. The second, Volume Delta, displays the difference of the ask volume minus the bid volume. These two studies will help me explain the third study, TT CVD.

|

| Figure 1: One-Minute December E-mini S&P 500 Chart |

In the opening one-minute period, 7,254 contracts are bought on the ask and 5,940 contracts are sold on the bid. There is a net market volume change, or volume delta, of +1,314 (7,254 minus 5,940). Since this is the beginning of the session and TT CVD is configured to reset at the beginning of a session, its value is simply the volume delta for this opening bar of +1,314.

Moving on to the next minute, in Figure 2 below, we see 2,111 contracts are bought on the ask and 3,444 contracts are sold on the bid. The volume delta is going to be negative here, since there were more market sellers than market buyers. The volume delta equals -1,333 for the second one-minute period of the day (2,111 minus 3,444).

|

| Figure 2: One-Minute December E-mini S&P 500 Chart |

TT CVD for the second bar is equal to the previous bar’s TT CVD value plus the volume delta. Continuing with our example, the previous bar’s TT CVD is +1,314, and the second bar’s volume delta is -1,333. Therefore, TT CVD equals -19 (1,314 minus 1,333). TT CVD continues to cumulate the volume delta for the remainder of the session and is a clear measurement for market order flow.

TT CVD and Daily Net Change

Now that we’ve explained how TT CVD is calculated, let’s compare the same setup for this study to the daily net change. TT CVD values trend similarly to the actual price data, since net market buying and selling should have a direct and correlated impact on the price. The larger the magnitude of TT CVD value, the greater the net change should be for the day.

Figure 3 below shows several days, with each day outlined and a net change value labeled. I used last traded price for each day, not the settle. For most days, if TT CVD is positive, so is the net change for the day. Likewise, if TT CVD is negative, so is the net change for the day. Sampling the last 90 trading days for this contract will show this statement is true for 67 days, or 74 percent of the time.

|

| Figure 3: 60-Minute December E-mini S&P 500 Chart |

The remaining 23 days sampled will be similar to December 4 and 5 in Figure 3. These days are generally neutral days with sideways action. The net change and TT CVD values are both near unchanged.This is one of the main reasons why the two values sometimes don’t line up with one another.

Now that you’ve seen how TT CVD works off more powerful market data points than just the open, high, low and close, I hope you agree that it is a true leading technical indicator. If you aren’t already using TT CVD, take the next step and add TT CVD to your X_STUDY charts so you can observe this leading technical indicator work in real time. And if you aren’t already using X_STUDY, what are you waiting for? It’s included free with all X_TRADER licenses. Learn more about X_STUDY here.

My next blog will look at another influential market data point that’s included in X_STUDY. Until then, plan the trade and trade the plan.

Tags: Charting

Note: If you’re not familiar with X_STUDY®, I encourage you to review the X_STUDY materials on our website. You’ll gain a solid understanding of this trader-centric charting application, which is fully integrated with TT’s X_TRADER® platform and provided to all X_TRADER users at no additional cost.

As the product manager for X_STUDY, TT’s charting and analytics application, I’d like to talk about constant volume bars. Constant volume bars build bars based on fixed volume instead of fixed time. There are several advantages to constant volume bars when compared to time-based bars.

Shorter time-based bars, like one-minute and five-minute bars, are great during the day when there are many market participants and the market tempo is fast. When market tempo slows and price action begins to consolidate, shorter time-based bars will continue generating bars as time passes. Too many of these time-based bars will inevitably flatten out your analytics, which can then generate whipsawed losing trades or take you out of a good trade.

A Case for Constant Volume Bars

A constant volume bar conforms to the market’s tempo. As the market tempo slows, so will the formation of new bars. As the tempo increases, so will the number of bars created. Volume bars are ideal for when events happen in the marketplace, too. For example, the release of an economic event at 1:15 can leave your five-minute bar waiting until 1:20, while the volume bars have already created four new bars in that five-minute window. These four faster-responding volume bars give your strategy more opportunity to react to the event that has just occurred in the market.

Likewise, who needs 12 five-minute bars from 12:15 to 1:15 before that economic number comes out when volume is light? Your analytics will be flat with time-based bars and won’t be able to help you make decisions. A volume chart in this same period might only form one bar. The concept of constant volume bars creates an intelligent bar that reacts to the market’s trading volume.

An Example

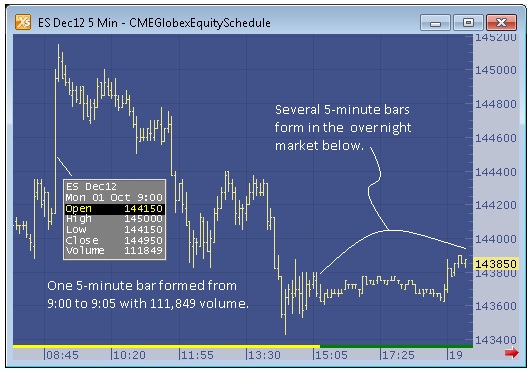

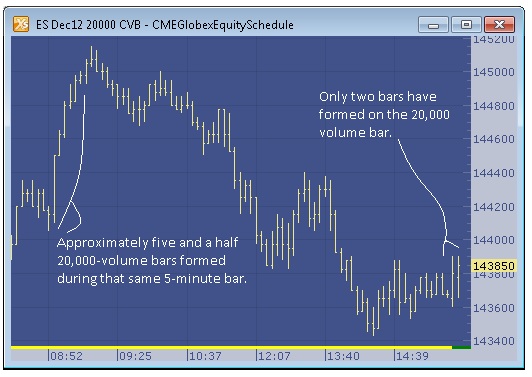

Let’s look at the scenario below, which uses the ES Dec12 contract from earlier this month. Compare a five-minute chart to a 20,000-volume chart. It will show advantages for when markets have both a fast and slow tempo. The five-minute bar chart shows a one-bar spike in the morning hours. The 9:00 to 9:05 a.m. bar in ES spikes to 1450.00. Comparing this bar to the 20,000-volume chart, we can see that approximately 5½ bars were formed on the constant volume bar chart during the same time.

Now look at the overnight market above. Here we can see more than forty bars have formed on the five-minute bar chart. This many bars will cause most technical indicators to flatten out and any automated system to start generating false signals, especially if the technical indicators are using fast values like a simple moving average of six bars. (I actually do not display all the bars here; there are more off to the right of the chart. You can tell this by the little red arrow at the bottom of the five-minute chart.)

The 20,000-volume bar has only produced two bars, with the second one still incomplete. At the time of the screenshot, the bar was only half complete, with around 11,000 volume. This example illustrates the improvement constant volume bars provide in both fast- and slow-moving markets.

In Closing

In my experience, I’ve found that constant volume bars can really improve analytics and help eliminate some of the whipsaws.This isn’t to say time-based charts are unnecessary. In fact, I myself still use time-based charts in much of my analysis. I don’t think I could give up daily charts; they are just too ingrained in my analysis. Rather, I’m simply suggesting that you might gain a little edge by looking at a combination of volume-based and time-based charts.Until next time, plan the trade and trade the plan.

Tags: Charting